Sok: dex with amm protocols

Summary of SoK: DEX with AMM Protocols

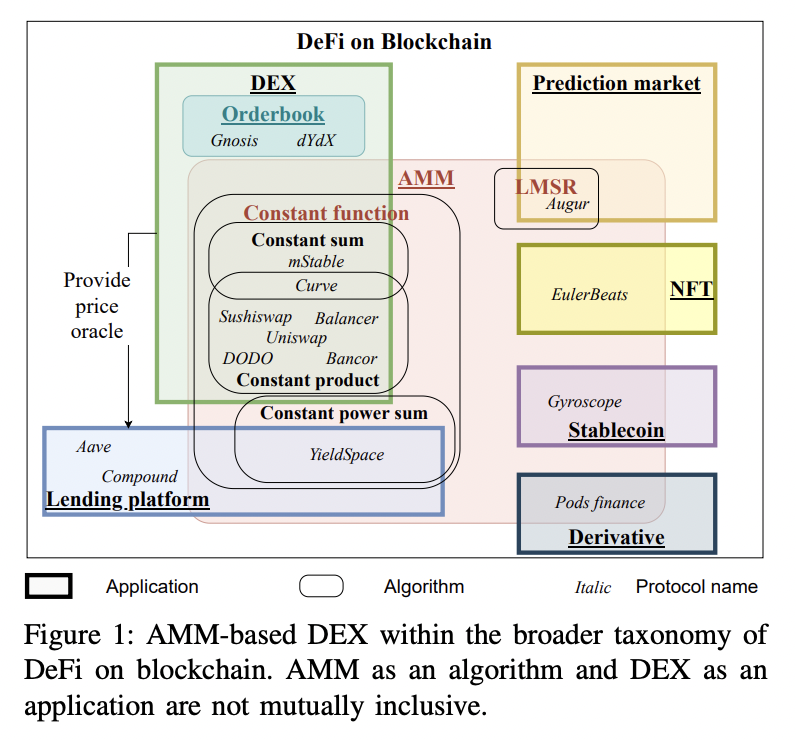

SoK: systematization of knowledge

AMM

Pros: Provides liquidity and encourage swapping assets

Cons: Slippage will easily occur. vulnerable to impermanent loss(divergence loss). Also has security issue

A lot of models were proposed to solve this issue, but there were mostly just the same.

The purpose of this paper is SoK of AMM-based DEX

Actors

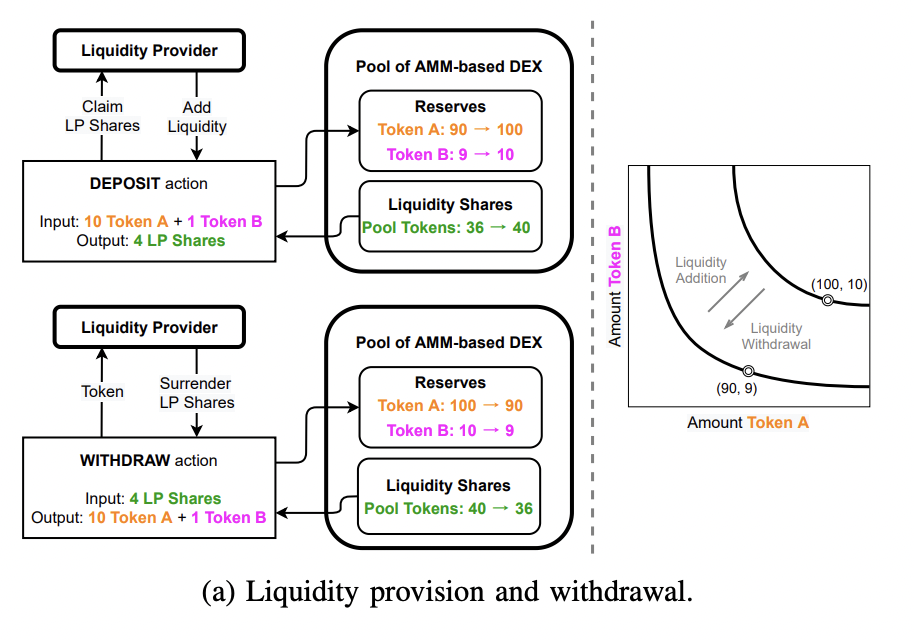

- Liquidity Providers

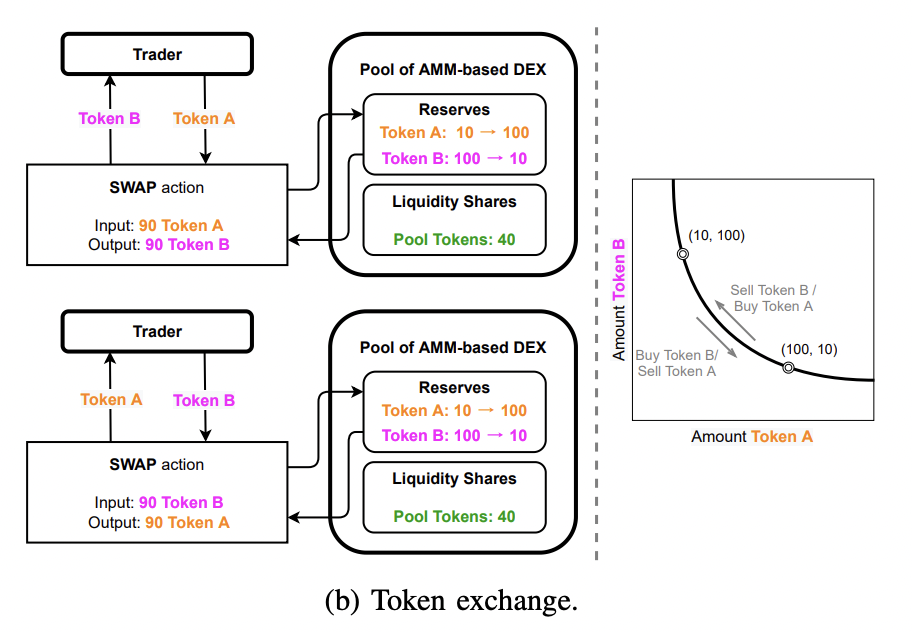

- Traders

- Protocol Foundation

Assets

- Risk assets

- Illiquidity, type of assets the DEX is designed for

- Base assets

- In some protocols, risk assets have to be designated with base assets

- Pool shares

- Liquidity shares, LP shares. Represents ownership in the portfolio of the assets within a pool

- Protocol tokens

- Governance token.

Dynamics

- Invariant properties

- conservation function. ex) CPMM

- Mechanisms

- asset swapping & liquidity provision/withdrawls

Economy

- Rewards

- Liquidity reward - Receive trading fees

- Staking reward - Rewards from staking pool shares or other tokens as part of an initial incentive program from a certain token protocol

- Governance right - rights to vote for proposals

- Security reward - bounty programs, auditing, etc.

- Explicit cost

- Liquidity withdrawal penalty

- Swap fee

- Gas fee

- Implicit cost

- Slippage

- Divergence loss(Impermenant loss)

State space representation

state \(\chi\)

\(\chi = ({\{r_k\}_{k=1,...,n}, \{p_k\}_{k=1,...,n}, C, \Omega})\)

\(r_k = quantity\ of\ token\ k\)

\(p_k = current\ spot\ price\ of\ token\ k\)

\(C = conservation\ function\ invariants\)

\(\Omega = collection\ of\ protocol\ hyperparameters\)

General rules of AMM-based DEX

- Price stays constant for pure liquidity provision and withdrawals

- Invariants of AMM pool stays constant for pure swapping

\((\{r_k\}, \{p_k\}, \mathcal{C}, \Omega) \xrightarrow{liquidity\ change} (\{r_k\}, \{p_k\}, \mathcal{C}', \Omega)\)

\((\{r_k\}, \{p_k\}, \mathcal{C}, \Omega) \xrightarrow{swap} (\{r_k'\}, \{p_k'\}, \mathcal{C}, \Omega)\)

- Cisproportionate addition or removal can be viewed as combination of proportionate reserve change plus asset swap

- Swap fees causes \(\mathcal{C}\) to change. It can be divided into swap and provision

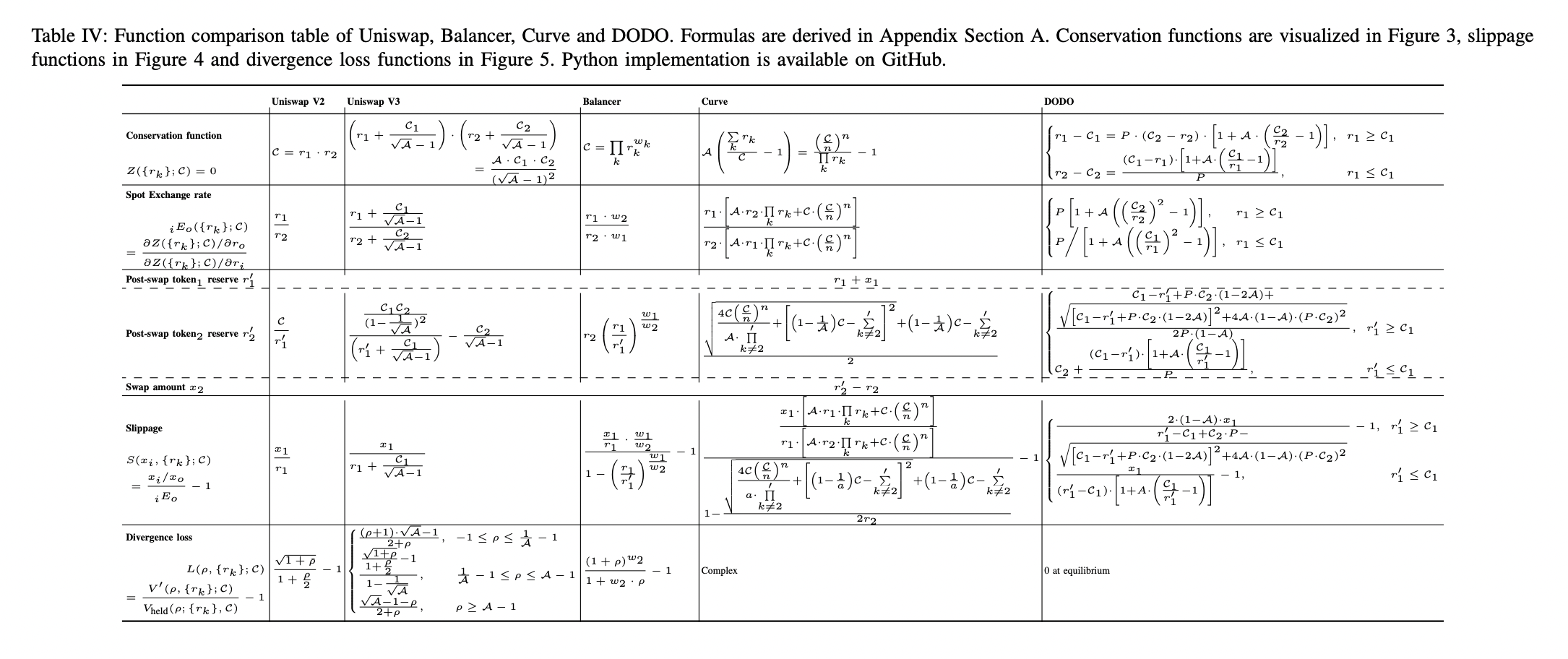

Generalized formulas

- Conservation function (bonding curve)

\(\mathcal{C} = C(\{r_k\})\)

conservation function for each token \((r_i - r_o)\) must be concave, nonnegative, nondecreasing

\(Z(\{r_k\};\mathcal{C}) = C(\{r_k\}) - \mathcal{C} = 0\)

here, \(\mathcal{C}\) is determined by initial liquidity provision.

For example, if AMM formula is \(XY = k\), then \(Z = XY - k,\ C(\{r_k\}) = XY,\ \mathcal{C} = k\) - Spot exchange rate

\(_iE_o(\{r_k\}; \mathcal{C}) = \dfrac{\partial Z(\{r_k\};\mathcal{C})/r_o}{\partial Z(\{r_k\};\mathcal{C})/r_i}\) -

Swap amount input \(x_i\), output \(x_o\)

a) Update reserve quantities

\(r_i':=R_i(x_i;r_i) = r_i + x_i\)

\(r_j' = r_j \ \forall j \neq i,o\)b) Compute new reserve quntity of token o

\(r_o' = R_o(x_i, \{r_k\}; \mathcal{C}) \Leftrightarrow Solving\ Z=0\)c) Compute swapped quntity

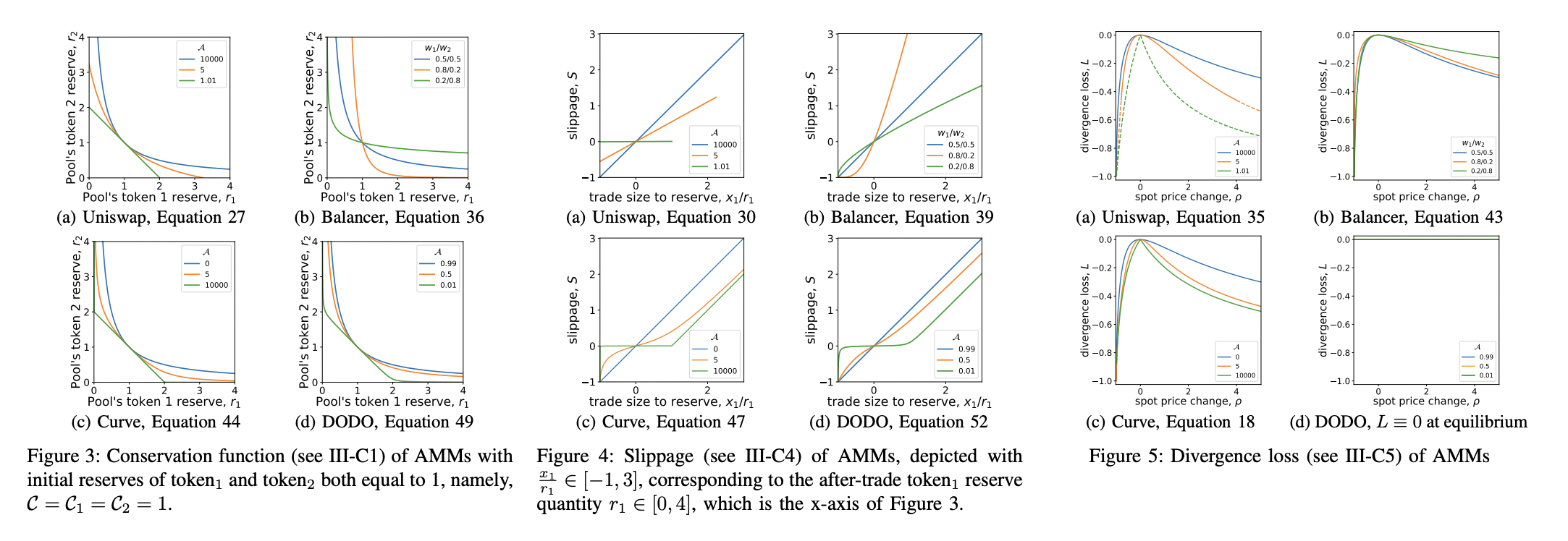

\(x_o := X_o(x_i, \{r_k\}; \mathcal{C}) = r_o - r_o'\) - Slippage \(S(x_i, \{r_k\}; \mathcal{C}) = \dfrac{x_i/x_o}{_iE_o} - 1\)

-

Divergence loss

value of token \(o\) is increased by \(\rho\) while others stay the same

token \(_i\) is a numeraire.

a) Calculate the original pool value

\(V(\{r_k\}; \mathcal{C}) = \sum_j{_iE_o(\{r_k\}; \mathcal{C}) \cdot r_j }\)b) Calculate the reserve value if held outside of the pool

\(V_{held}(\rho; \{r_k\}, \mathcal{C}) = V(\{r_k\}; \mathcal{C}) + [_iE_o(\{r_k\}; \mathcal{C}) \cdot r_o] \cdot \rho\)c) Obtain re-balanced reserve quantities

\(\rho = \dfrac{_jE_o(\{r_k'\};\mathcal{C})}{_jE_o(\{r_k\};\mathcal{C})} -1\)

\(Z(\{r_k'\};\mathcal{C}) = 0\)

\(r_k' = R_k(\rho,\{r_k\};\mathcal{C})\)d) Calculate the new pool value

\(V'(\rho,\{r_k'\}; \mathcal{C}) = \sum_j{_iE_j(\{r_k'\};\mathcal{C}) \cdot r_j'}\)e) Calculate the divergence loss

\(L(\rho, \{r_k'\}; \mathcal{C}) = \dfrac{V'(\rho, \{r_k'\}; \mathcal{C})}{V_{held}'(\rho, \{r_k'\}; \mathcal{C})} -1\)

Formulas of major AMM-based Dex

Uniswap V2

a) Conservation function

\(\mathcal{C} = r_1 \cdot r_2\)

b) Spot exchange rate

\(_1E_2 = \dfrac{r_1}{r_2}\)

c) Swap amount

\(r_1' = r_1 + x_1\)

\(r_2' = \dfrac{\mathcal{C}}{r_1'}\)

\(x_2 = r_2 - r_2'\)

d) Slippage

\(S(x_1) = \dfrac{x_1/x_2}{_1E_2} -1 = \dfrac{x_1}{r_1}\)

e) Divergence loss

\(\dfrac{V}{2} = V_1 = V_2 = r_1\)

\(V_{held} = V + V_2 \cdot \rho = r_1 \cdot (2 + \rho)\)

\(\dfrac{V'}{2} = V_1' = V_2' = r_1' = r_1 \cdot \sqrt{1 + \rho}\)

Note that \(r_2' = \dfrac{r_2}{\sqrt{1 + \rho}}\) and \(p' = \dfrac{(1 + \rho)r_1}{r_2}\)

\(L(\rho) = \dfrac{V'}{V_{held}}-1 = \dfrac{\sqrt{1 + \rho}}{1 + \dfrac{\rho}{2}}-1\)

Uniswap V3

a) Conservation function

Suppose a user supplies \(\mathcal{C_1}\) token 1 and \(\mathcal{C_2}\) token 2

His liquidity is only provided for swapping within a specific range of exchange rates: \([\dfrac{\mathcal{C_1}}{\mathcal{C_2}\mathcal{A}}, \dfrac{\mathcal{C_1}\mathcal{A}}{\mathcal{C_2}}]\) where \(\mathcal{A} > 1\) and initial exchange rate is \(\dfrac{\mathcal{C_1}}{\mathcal{C_2}}\)

\(r_1^{equiv} = \dfrac{\mathcal{C_1}}{1-\dfrac{1}{\sqrt{\mathcal{A}}}}\ and\ r_2^{equiv} = \dfrac{\mathcal{C_2}}{1-\dfrac{1}{\sqrt{\mathcal{A}}}}\)

Conservation function looks like this:

\([r_1 + (r_1^{equiv} - \mathcal{C_1})] \cdot [r_2 + (r_2^{equiv} - \mathcal{C_2})] = r_1^{equiv} \cdot r_2^{equiv}\)

\((r_1 + \dfrac{\mathcal{C_1}}{\sqrt{\mathcal{A}}-1}) \cdot (r_2 + \dfrac{\mathcal{C_2}}{\sqrt{\mathcal{A}}-1}) = \dfrac{\mathcal{A} \cdot \mathcal{C_1} \cdot \mathcal{C_2}}{(\sqrt{\mathcal{A}}-1)^2}\)

b) Exchange rate

\(_1E_2 = \dfrac{r_1 + \dfrac{\mathcal{C_1}}{\sqrt{\mathcal{A}}-1}}{r_2 + \dfrac{\mathcal{C_2}}{\sqrt{\mathcal{A}}-1}}\)

c) Swap amount

\(r_1' = r_1 + x_1\)

\(r_2' = \dfrac{\mathcal{C_1}\mathcal{C_2}}{(1-\dfrac{1}{\sqrt{\mathcal{A}}})^2} / (r_1' + \dfrac{C_1}{\sqrt{\mathcal{A}}-1}) - \dfrac{\mathcal{C_2}}{\sqrt{\mathcal{A}}-1}\)

\(x_2' = r_2 - r_2'\)

d) Slippage

\(S(x_1) = \dfrac{x_1/x_2}{_1E_2} -1 = \dfrac{x_1}{r_1 + \dfrac{\mathcal{C_1}}{\sqrt{\mathcal{A}}-1}}\)

e) Divergence loss

\[L(\rho) = \dfrac{V'}{V_{held}}-1 \\ = \begin{cases} \dfrac{(\rho +1 ) \cdot \sqrt{\mathcal{A}}-1}{2+\rho},&-1 \le \rho \le \dfrac{1}{\mathcal{A}}-1 \\ \dfrac{\dfrac{\sqrt{1+\rho}}{1+\dfrac{\rho}{2}}-1}{1-\dfrac{1}{\sqrt{\mathcal{A}}}}, & \dfrac{1}{\mathcal{A}} -1 \le \rho \le \mathcal{A}-1 \\ \dfrac{\sqrt{\mathcal{A}}-1-\rho}{2+\rho}, & \rho \ge \mathcal{A}-1 \end{cases}\]Balancer

a) Conservation function

\(\prod_k r_k^{w_k}\)

b) Spot exchange rate

\(_1E_2 = \dfrac{r_1 \cdot w_2}{r_2 \cdot w_1}\)

c) Swap amount

\(r_1' = r_1 + x_1\)

\(r_2' = r_2(\dfrac{r_1}{r_1'})^{\dfrac{w_1}{w_2}}\)

\(x_2 = r_2 - r_2'\)

d) Slippage

\(S(x_1) = \dfrac{x_1/x_2}{_1E_2} -1 = \dfrac{\dfrac{x_1}{r_1} \cdot \dfrac{w_1}{w_2}}{1 - (\dfrac{r_1}{r_1'})^{\dfrac{w_1}{w_2}}}-1\)

e) Divergence loss

\(V = \dfrac{V_1}{w_1} = \dfrac{V_2}{w_2} = \dfrac{V_k}{w_k} = \dfrac{r_1}{w_1}\)

\(V_{held} = V + V_2 \cdot \rho = V \cdot(1 + w_2 \cdot \rho)\)

\(V' = \dfrac{V_1'}{w_1} = \dfrac{r_1'}{w_1} = \dfrac{r_1 \cdot (1 + \rho)^{w_2}}{w_1} = V \cdot (1 + \rho)^{w_2}\)

\(L(\rho) = \dfrac{V'}{V_{held}} -1 = \dfrac{(1+\rho)^{w_2}}{1 + w_2 \cdot \rho} -1\)

Curve

a) Conservation function

\(A(\dfrac{\sum_k r_k}{\mathcal{C}} -1) = \dfrac{(\dfrac{\mathcal{C}}{n})^n}{\prod_k r_k} -1\)

b) Spot exchange rate

\(Z(r_1, r_2) = \dfrac{(\dfrac{\mathcal{C}}{n})^n}{r_1r_2\prod_{k\ne1,2} r_k} -1 -\mathcal{A}(\dfrac{r_1 + r_2 + \sum_{k\ne1,2} r_k}{\mathcal{C}}-1)\)

\(_1E_2 = \dfrac{\partial Z(r_1, r_2) / \partial r_2}{\partial Z(r_1, r_2) / \partial(r_1)} = \dfrac{r_1 \cdot [\mathcal{A}\cdot r_2 \cdot \prod_k r_k + \mathcal{C} \cdot (\dfrac{\mathcal{C}}{n})^n]}{r_2 \cdot [\mathcal{A}\cdot r_1 \cdot \prod_k r_k + \mathcal{C} \cdot (\dfrac{\mathcal{C}}{n})^n]}\)

c) Swap amount

\(r_1' = r_1 + x_1\)

\(r_2' = \dfrac{\sqrt{\dfrac{4\mathcal{C}(\dfrac{C}{n})^n}{\mathcal{A} \cdot \prod_{k \ne 2}^{'}} + [(1 - \dfrac{1}{\mathcal{A}})\mathcal{C} - \sum_{k \ne 2}^{'}]^2} + (1 - \dfrac{1}{\mathcal{A}})\mathcal{C} - \sum_{k \ne 2}^{'}}{2}\)

\(x_2 = r_2 - r_2'\)

where \(\prod_{k \ne 2}^{'} = r_1' \cdot \prod_{k \ne 1,2} r_k \:\) and \(\sum_{k \ne 1,2}^{'} = r_1' + \sum_{k \ne 1,2}r_k\)

d) Slippage

\[S(x_1) = \dfrac{x_1 / x_2}{_1E_2} -1 \\ = \dfrac{\dfrac{x_1 \cdot [\mathcal{A} \cdot r_1 \prod_k r_k + \mathcal{C} \cdot (\dfrac{\mathcal{C}}{n})^n]}{r_1 \cdot [\mathcal{A} \cdot r_2 \prod_k r_k + \mathcal{C} \cdot (\dfrac{\mathcal{C}}{n})^n]}}{1 - \dfrac{\sqrt{\dfrac{4\mathcal{C}(\dfrac{\mathcal{C}}{n})^n}{a\cdot\prod_{k\ne 2}^{'}} + [(1 - \dfrac{1}{a})\mathcal{C - \sum_{k \ne 2}^{'}}]^2}+ (1 - \dfrac{1}{a})\mathcal{C} - \sum_{k \ne 2}^{'}}{2r_2}}\]DODO

a) Spot exchange rate

b) Conservation function

\[r_1 - \mathcal{C_1} = \int_{r_2}^{\mathcal{C_2}}P[1+\mathcal{A}((\dfrac{\mathcal{C_2}}{\delta})^2 -1)]d\delta \\ = P \cdot (\mathcal{C_2} - r_2) \cdot [1 + \mathcal{A} \cdot (\dfrac{\mathcal{C_2}}{r_2}-1)], \,\: r_1 \ge \mathcal{C_1}\] \[r_2 - \mathcal{C_2} = \int_{r_1}^{\mathcal{C_1}}\dfrac{1+\mathcal{A}((\dfrac{\mathcal{C_1}}{\delta})^2 -1)}{P}d\delta \\ = \dfrac{(\mathcal{C_1} - r_1) \cdot [1 + \mathcal{A} \cdot (\dfrac{\mathcal{C_1}}{r_1}-1)]}{P}, \,\: r_1 \le \mathcal{C_1}\]c) Swap amount

\(r_1' = r_1 + x_1\)

d) Slippage

\[S(x_1) = \begin{cases} \dfrac{2 \cdot (1 - \mathcal{A} \cdot x_1)}{r_1' - \mathcal{C_1} + \mathcal{C_2} \cdot P - \sqrt{[\mathcal{C_1}-r_1'+P\cdot \mathcal{C_2} \cdot (1 - 2\mathcal{A})]^2 + 4\mathcal{A} \cdot (1 - \mathcal{A}) \cdot (P \cdot \mathcal{C_2})^2} } -1, & r_1' \ge \mathcal{C_1} \\ \dfrac{x_1}{(r_1' - \mathcal{C_1}) \cdot [1 + \mathcal{A} \cdot (\dfrac{\mathcal{C_1}}{r_1'} -1)]} -1, & r_1' \le \mathcal{C_1} \end{cases}\]